Envista 2026 Q1: Sales Revenue of $706 Million, Core Revenue Up 9.5% Year-over-Year [SOURCE] Envista reported sales revenue of $706 million for the first quarter of 2026, with core revenue i…

|

| Source: Envista 2026 First Quarter Performance Report |

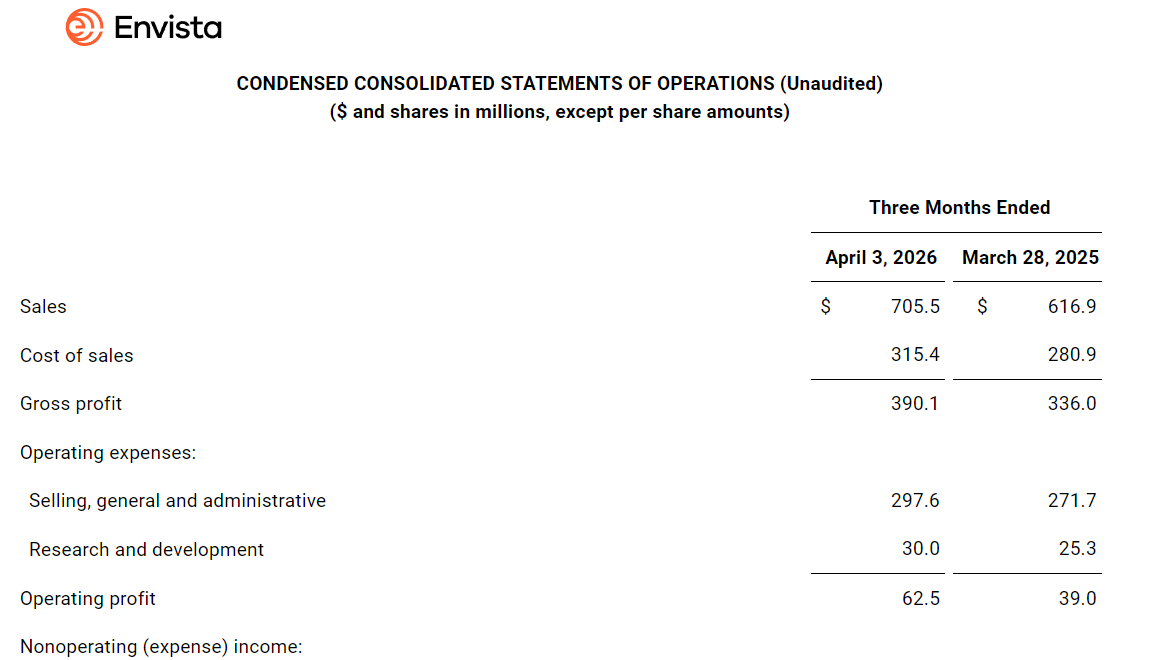

DentalGoodNews|On May 6, 2026, Envista Holdings Corporation released its first-quarter 2026 earnings report. The report data shows that the company's single-quarter sales for the first quarter were $705.5 million (approximately RMB 4.804 billion), a year-over-year increase of 14.4%, with core sales growth of 9.5% excluding the impact of foreign exchange and acquisitions; adjusted diluted earnings per share were $0.36, up 50.0% year-over-year; adjusted EBITDA margin was 14.0%, an improvement of 120 basis points from 12.8% in the same period of 2025.

CEO Paul Keel stated that all major businesses achieved growth in 2026, with core revenue growth of 9.5% translating into a 25% increase in adjusted EBITDA and a 50% increase in earnings per share.

|

| Source: Envista 2026 First Quarter Performance Report |

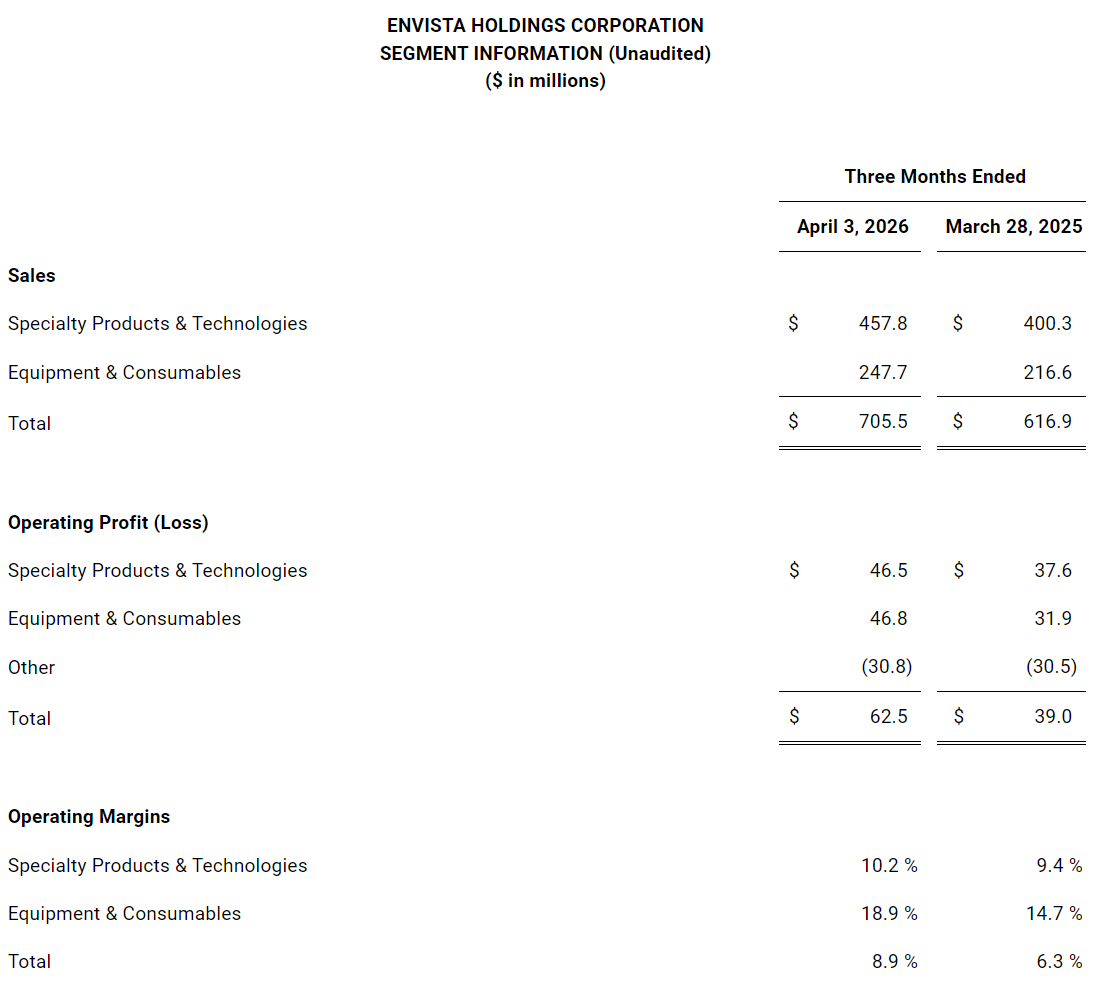

By business segment, the Specialty Products & Technologies segment (covering Nobel Biocare and Implant Direct dental implants, as well as Ormco and Spark clear aligners and other orthodontic businesses) achieved sales of $457.8 million (approximately RMB 3.118 billion), a year-over-year increase of 14.4%, with core growth of 8.4% and an adjusted operating margin of 14.5% (14.1% in Q1 2025). Within this segment, both Spark and B&W achieved double-digit growth, while Implants showed mid-single-digit growth outside of China, with a short-term decline in the Chinese market to align with Volume-Based Procurement (VBP) policies. The Equipment & Consumables segment (covering DEXIS imaging diagnostics and Kerr consumables) achieved sales of $247.7 million (approximately RMB 1.687 billion), a year-over-year increase of 14.4%, with core growth of 11.5% and an adjusted operating margin of 21.0% (18.1% in Q1 2025). Both diagnostic and consumable products achieved growth in North America and Western Europe.

|

| Source: Envista 2026 First Quarter Performance Report |

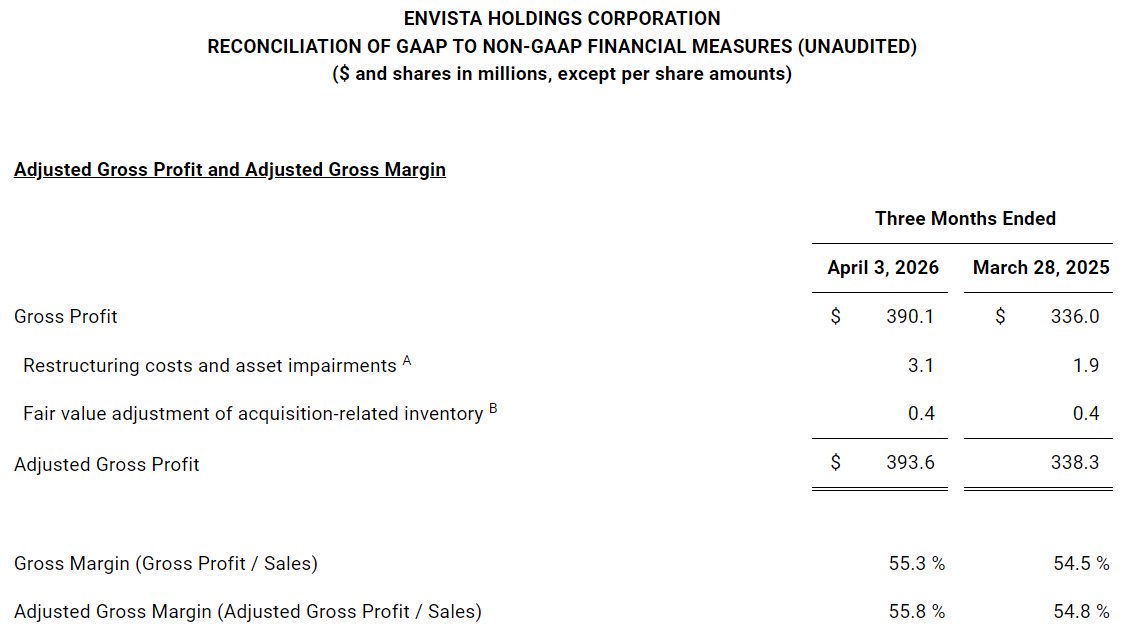

In terms of profitability, GAAP gross margin was 55.3% (54.5% in Q1 2025), and adjusted gross margin was 55.8% (54.8% in Q1 2025), an improvement of approximately 100 basis points. The gross margin improvement was primarily attributed to the ongoing optimization of the Envista Business System (EBS). R&D expenses were $30 million (approximately RMB 204 million). The company stated that R&D and sales and marketing investments achieved double-digit growth in the quarter.

|

| Source: Envista 2026 First Quarter Performance Report |

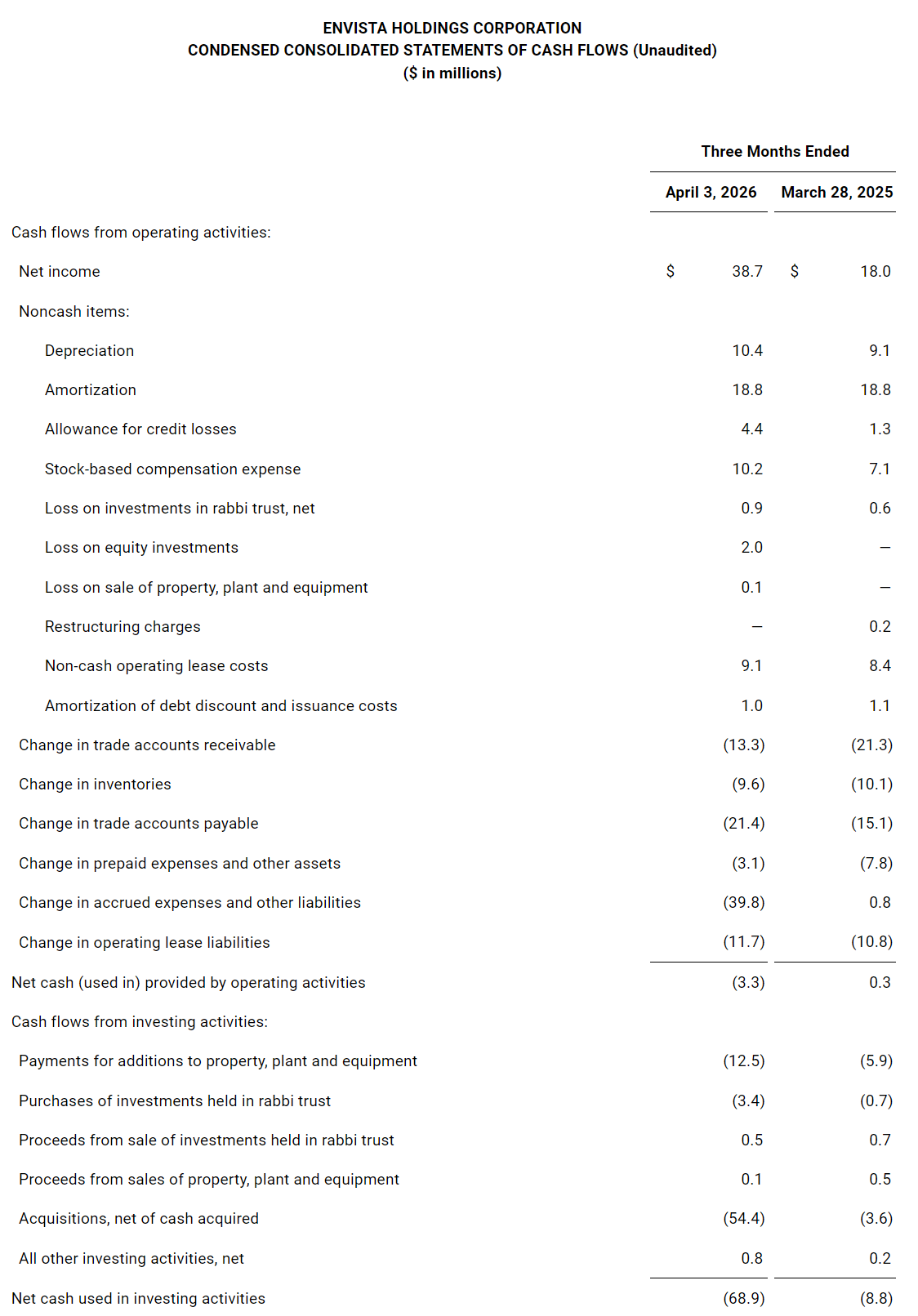

In terms of cash flow, net cash outflow from operating activities in the quarter was $3.3 million (approximately RMB 22.47 million) (net inflow of $0.3 million in Q1 2025), capital expenditures were $12.5 million (approximately RMB 85.13 million) (Q1 2025: $5.9 million), and M&A expenditures were $54.4 million (approximately RMB 371 million). Cash and cash equivalents at the end of the period were $1.0828 billion (approximately RMB 7.374 billion) (end of 2025: $1.2117 billion, approximately RMB 8.252 billion).

During the quarter ending April 3, 2026, the company repurchased a total of 1.6 million shares, amounting to approximately $43 million (approximately RMB 293 million). At the end of the quarter, the company had approximately $41 million remaining under its existing repurchase authorization. The Board of Directors authorized a new $300 million (approximately RMB 2.043 billion) share repurchase program, effective through December 31, 2029.

For 2026, the company expects core sales growth of 2%-4%, adjusted EBITDA growth of 7%-13%, adjusted diluted earnings per share of $1.35-$1.45 (approximately RMB 9.19-9.87), and a free cash flow conversion rate of approximately 100%.

| About DGN:DentalGoodNews (DGN) is a trusted professional media platform dedicated to the global dental industry. We deliver in-depth coverage of corporate news, policy & regulation, investment & funding, and clinical frontiers — serving dental institutions, device manufacturers, investors, and industry researchers worldwide. Contact us: haodeya@dongxizixun.com |

;){kind=link}